Life Rights vs Sectional Title: A Retiree's Guide

Your definitive guide to securing real wealth and avoiding the hidden risks in retirement property.

For retirees in Cape Town’s Northern Suburbs, the choice between Life Rights vs Sectional Title is more than a property decision.

It is the difference between owning a growing asset and holding a high-risk contract that could leave your estate with nothing.

Both models have clear benefits and serious risks, and understanding them fully is vital before making a commitment.

Understanding a Life Right agreement

A Life Right gives you the right to live in a retirement village unit for the rest of your life, while ownership remains with the developer.

Key features of Life Rights:

- Right of occupation, not property ownership.

- Refund of a percentage of the original purchase price to your estate.

- Levies are all-inclusive, covering maintenance, rates, and services.

- Legal protections under the Housing Development Schemes for Retired Persons Act.

Advantages:

- Lower upfront costs: No transfer duty, VAT, or bond registration.

- Predictable levies: Monthly payments are fixed and include most costs.

- No maintenance responsibility: Developer handles repairs and upkeep.

- Fast occupation: No deeds office delays.

Disadvantages:

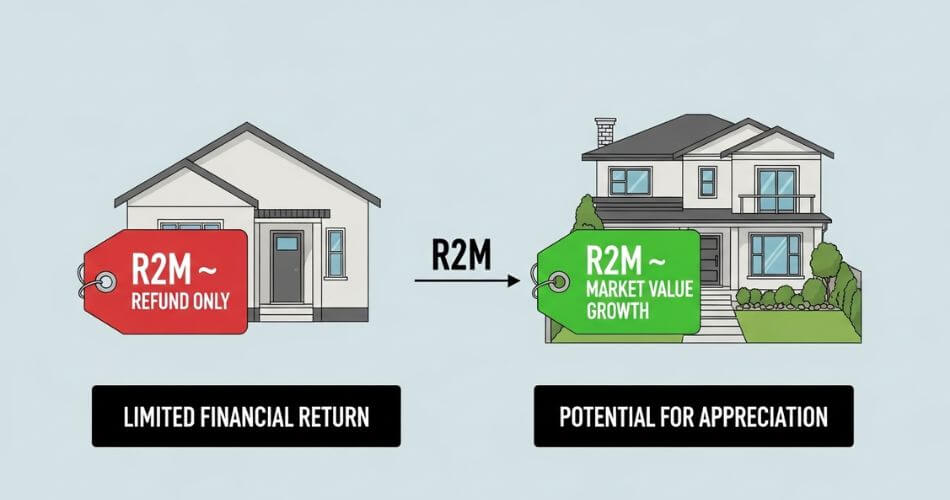

- No capital growth benefit: Appreciation belongs to the developer.

- Estate payout delays: Refund only after the unit is resold.

- Developer insolvency risk: A 2024 court ruling means buyers rank as unsecured creditors if the developer fails.

- Limited control: You cannot choose when to resell or adjust your exit terms.

Understanding Sectional Title ownership

Sectional Title ownership gives you a title deed to your unit plus a share of the communal property.

Key features of Sectional Title:

- Full ownership with a registered title deed.

- The property can be financed, sold, or inherited.

- Voting rights in the body corporate.

- Capital appreciation belongs to the owner.

Advantages:

- Capital growth on property: Your estate benefits from full market appreciation.

- Control over resale: You choose when and how to sell.

- Wealth preservation: Asset can be passed on to heirs.

- Legal protections: Stronger safeguards compared to Life Rights.

Disadvantages:

- Higher upfront costs: Transfer duty, VAT, and conveyancing fees apply.

- Monthly variability: Levies exclude rates, taxes, and utilities.

- Maintenance responsibility: Owners cover internal upkeep.

Special levies: Body corporates can raise additional charges for major repairs.

The Financial Reality: Costs and Capital growth on property

The financial impact of choosing between a Life Right agreement and Sectional Title ownership is best understood by looking at three stages:

- What you pay upfront.

- What you pay each month.

- What your estate eventually receives back.

Upfront Costs – A Life Right typically requires less cash at the start. Using a R2 million property as an example:

- Life Rights: About R2,005,000 in total, with no transfer duty, no VAT, and minimal conveyancing fees.

- Sectional Title: Between R2,125,000 and R2,325,000, once transfer duty (R100,000), possible VAT, and higher conveyancing costs are added.

This means a Life Right can save you between R120,000 and R320,000 upfront compared with buying a Sectional Title.

Ongoing Monthly Costs

Levies differ not just in amount but in what they include.

- Life Right levies: R4,500–R12,000+, depending on unit size. These are all-inclusive, covering rates, taxes, water, security, and general maintenance. Importantly, developers are not allowed to raise special levies.

- Sectional Title levies: R2,500–R4,500 for a one-bedroom, but this excludes rates and taxes, water, and electricity, which must be paid separately. Owners are also exposed to special levies if large repairs or upgrades are required.

So while Sectional Title appears cheaper month-to-month, the extra charges and potential special levies can make costs less predictable.

The Final Payout To Your Estate – This is where the two models diverge most sharply.

- Life Rights: Your estate usually receives 70–100% of the original purchase price, with no share in capital growth. The payout only happens once the developer has resold the unit, and until then, your estate must continue paying levies. Deduction examples include:

- Featherwood: 95% refund, minus contributions to levy and care funds, plus up to 3% for repairs.

- Methodist Homes: 50% of the original purchase price plus 50% of the cost of improvements.

- Auria: Declining refund scale, from 95% in year one down to 80% after four years.

These structures mean your heirs may receive less than your original outlay, and payment may be delayed.

- Sectional Title: Your estate receives the full market value of the property at the time of sale, including all capital growth. The executor controls the timing of the sale, and proceeds are available as soon as the property transfer is complete.

Bottom Line

Life Rights reduce your initial costs and simplify monthly payments but offer no capital growth and can delay or diminish your estate’s payout.

Sectional Title requires more upfront and variable ongoing expenses, yet it protects your wealth by delivering market-based growth and full control over resale.

The Hidden Dangers: Retirement property risks

Retirement property is not risk-free, and ignoring these risks can cost your estate dearly.

Risks with Life Rights:

- Developer insolvency: A 2024 court ruling means buyers rank as unsecured creditors if the developer fails, because a Life Right is legally considered a loan to the developer, not a property purchase.

- Delayed refunds: Your estate may wait months, or even years, for repayment until a new buyer is found.

- Limited legal recourse: Once funds are transferred to a developer, recovery through legal channels is nearly impossible.

Risks with Sectional Title:

- Special levies: Unexpected repair projects can demand large once-off payments.

- Maintenance obligations: Internal upkeep and renovations are your responsibility.

- Market dependence: Sale prices depend on broader property market conditions.

A Look at Retirement villages in the Northern Suburbs

The Northern Suburbs of Cape Town offer a variety of retirement developments, but it is essential to distinguish between Life Right schemes and Sectional Title ownership, as the financial outcomes differ significantly.

Verified Life Right Villages:

Oasis Life Clara Anna Fontein (Durbanville)

Onze Molen (Durbanville)

Manor on Lords Walk (Durbanville)

Vygeboom (Durbanville)

Starckwood Retirement Village (Brackenfell)

Panorama Palms (Panorama)

Eden Park (Kuils River)

Verified Sectional Title Villages:

Klaradyn Retirement Village (Brackenfell)

Buh-Rein Retirement Village (Kraaifontein)

- La Rochelle Retirement Village in Bellair

While there are several well-established retirement villages in the Northern Suburbs, the key consideration for buyers is not only location or amenities but also the ownership model itself.

Confirming whether a development operates on a Life Right agreement or Sectional Title ownership is vital, as this decision has lasting consequences for both your monthly costs and the value ultimately returned to your estate.

Conclusion

The choice between Life Rights vs Sectional Title is ultimately about control, inheritance, and risk.

Life Rights offer immediate savings, predictable levies, and convenience, but at the cost of forfeiting capital growth and exposing your estate to developer risk.

Sectional Title requires higher upfront investment but secures long-term wealth, inheritance, and ownership protections.

Final word: If your goal is stability and minimal responsibility, Life Rights may suit. If preserving and growing your estate is important, Sectional Title ownership is the stronger path.

Before making your decision, consult a trusted property strategist and review the financial health of the specific retirement village. The right choice today can safeguard your estate and bring clarity to your retirement years.

About the Author

Andre Swart is a respected leader in Brackenfell real estate with over 20 years of results-driven experience. Through his platform, “Andre Swart Inspires,” he moves beyond simple property sales to share the proven mindset, strategies, and habits that build lasting success.

Grounded in integrity, Andre’s mission is to mentor the next generation of top agents and provide homeowners with the trusted guidance they deserve.